My plan for this year is to consistently buy into REITS:

(one REIT per every 2 months worth at least around $1,500- $3,000 per buy to keep cost slightly lower)

Therefore, by the end of this year, I would/should have achieved the purchase of 6 REITS hopefully within the amount of $12,000-$15,000.

My constraints and my decisions:

1. Cost vs Consistency/Discipline:

My first year of investment would likely see me incur a higher cost per transaction. This is largely due to the lack of capital (which shall not be my excuse anymore). I will therefore come up with a plan that emphasize on Discipline and Consistency for this first year. For a workaround, I have decided that for each REIT I purchase, I would want to keep my costs incurred to within 3% or below per transaction. By identifying REITS that fit into my investment appetite mainly growth and dividends REITS that are manageable for my capital outlay, I should achieve an overall Dividend Yield of 2-4% for this first year.

My major weakness in life has been on the issue of discipline, therefore I have decided to set aside $1,500 - $1,800 a month to buy a REIT. Dollar-cost-averaging, since my first year is just to get the discipline to do my homework and invest consistently.

2. Imperfect knowledge of the Market and the REITS I'm buying into:

I shall refrain from buying in bulk also because of my imperfect knowledge of the market. It would be good for me to practice my fundamental analysis and see how they turn out in a year, whether I was right/wrong. I am still new and I cannot possibly know everything but I have to make smart guesses and calculated risks along the way.

It would also allow me to buy into different sectors of REITS and learn more about how they function as a whole to market movements and sentiments.

3. Unfamiliarity with the tools I'm using at the moment:

I'm currently using some Dividends trackers made by others, a few websites that source REITS news and I'm also new to how DBS vickers/CDP works. Time will tell which of these tools I'm using are good/more reliable than others or not. I would likely take time to explore the functions and various information available to me.

As of the time I am buying into the REIT, I have not studied every single piece of information put to me by the software, websites as the amount of information is huge. This will likely need some digestion on my side.

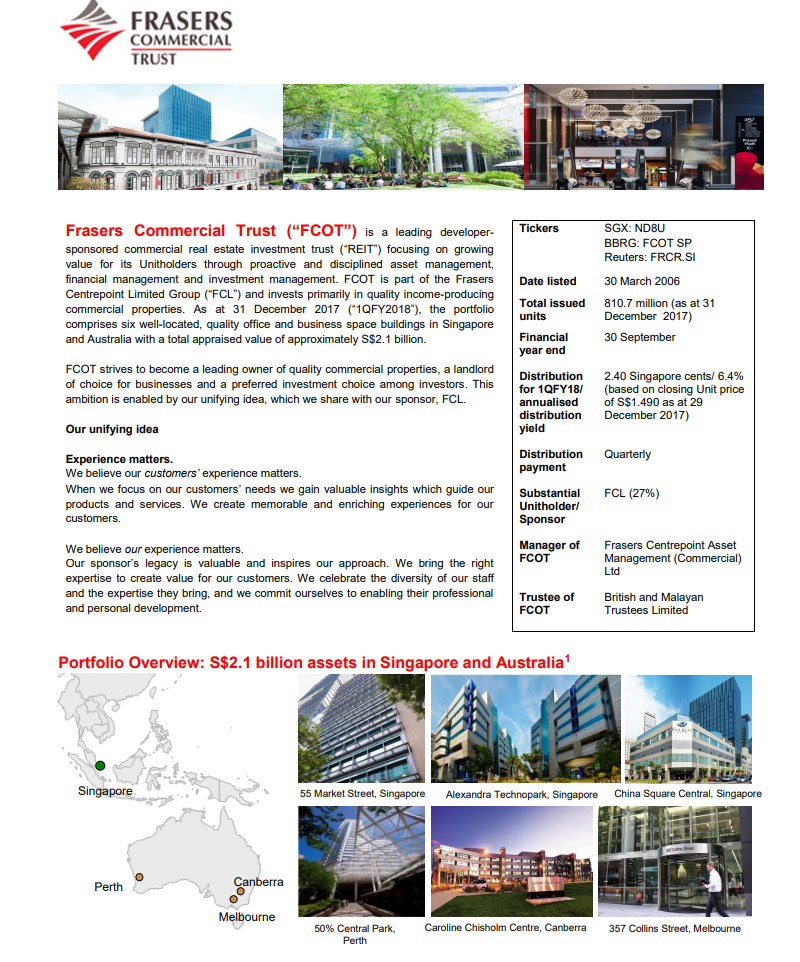

My first REIT: Frasers Commercial Trust (FCOT)

As of the time I studied the REITs, I had quite a few REITs I had identified based on my fundamental analysis.

My criterias were:

1. Promising Growth

2. Consistent Dividends (track record)

3. Fundamentals of the company (assets short-term to long-term)

I had eliminated a few like Lippo Malls Trust which was favored alot by retail investors. (I might re-look again at this REIT)

Indonesia is an emerging market and this REIT has given consistently high dividend yield. On the surface it looks like a good REIT. However, even as their assets are mainly retail malls, their net asset value has not increased much over the years as the underlying property and assets is stagnated/depreciating due to the Rupiah/ market condition.

Comparing apple for apple, CapitaR China Trust (I will certainly be looking at this again) has that same growth potential but the RMB is in a much stronger shape backed by the purchasing power of the chinese and situated in much more populated areas with much more solid big brand tenants like Uniqulo, Zara, watsons and Aeon.

Anyway, back to Frasers Commercial Trust:

Source: Frasers Commercial Trust Website

For me, this REIT has been strong fundamentally although the dividend Yield is not the best it has been delivering consistency. Its Nett assets have also been increasing in value over the years. 50% of the REIT comprises of Australia properties.

In Singapore, the China Square tenant revenue has taken a hit due to upgrading from 2016 projected to end in mid 2019 and the loss of HP as a major tenant caused a slightly lower performance in this quarter. But other than this, the other tenanted properties are doing well with high tenancy rate.

For Australia side, I am honestly not too familiar with the Aussie market but it has seen a slight dip due to the weakening Aussie dollar but is also not doing too bad. More homework and due diligence would be needed before I make an opinion of the Australia side of things but from the fundamentals it is strong enough to convince me of its mid to long term growth. FCOT is also in a joint venture currently to purchase Farnborough Business Park which has a long weighted average lease expiry (98.1% leased) in London, UK.

Update:

FCOT in numbers

My Key Indicators

| FY2014 | FY2015 | FY2016 | FY2017 | LTM Ending | |

| 30-Sep-14 | 30-Sep-15 | 30-Sep-16 | 30-Sep-17 | 31-Dec-17 |

|

118.838 | 142.187 | 156.497 | 156.551 | 152.193 | |

Gross Profit

|

90.554 | 101.868 | 115.614 | 113.843 | 109.562 | |

| GP/TR% | 76.1995321 | 71.6436805 | 72.7194333 | 71.9888563 |

| Dividend Yield (based on last stock price) |

6.83098592 |

Net PP&E

|

1,824.94 | 1,954.88 | 1,989.37 | 2,070.92 | 2,054.60 |

|

76.2 | 71.644 | 73.876 | 72.719 | 71.989 | |

Operations

|

82.01 | 88.574 | 101.786 | 96.824 | 86.155 |

Investing

|

-3.454 | -197.286 | -3.32 | -5.439 | -26.506 |

Financing

|

-73.578 | 124.185 | -89.397 | -88.356 | -85.432 |

|

2.177 | 2.011 | 0.363 | 0.39 | 0.304 | |

GEARING

|

34.80 | ||||

|

63.522 | 60.847 | 61.012 | 58.234 | 58.398 | |

|

3.854 | 4.029 | 4.149 | 4.112 | 3.936 | |

EBITDA

|

0.034 | 13.541 | 15.177 | -1.909 | -6.121 |

As of 19/2/2018:

1,000 shares bought at $1.440

Till next time,

K.C.

---------------------------------------------

Disclaimer: The above information are for personal discussion purposes only and do not constitute financial advice. Do conduct your due diligence before making any financial decision. "30 Year Old Investor" shall not be liable for any loss or damage of any kind arising from the result of your reliance of the information contained on this site.

&via=stc_network)

No comments:

Post a Comment