Hello fellow friends and investors!

Sorry, I have not been updating the blog as much as I would have liked. Hope everyone is still coping well in this Covid-19 pandemic season. I miss everyone and indeed miss having the luxury of time to sit down, study stocks, read books and craft blog posts.

I still do post and share articles I find useful on facebook! Click to follow the following to receive updates:

- 30yearoldinvestor Facebook Page: https://www.facebook.com/30yroldinvestor

- REIT Community (Facebook group): I am also partnering with Reit-tirement blog and other bloggers to share ideas at: https://www.facebook.com/groups/1397925937071525/

What changed in the last 7 months? (work wise)

My last blog post happened during the "crash" back in March. That coincided with a working from home implementation by my company.

I had thought that working from home would mean that I would have more time at home to "do my own things". As it turns out, I misjudged the situation.

1. Resilient Business and Projects = Extended working hours

Even though with Covid-19, at work I was expected to continue to run projects (but with reduced manpower) to fulfill expectations. The overall effect was that the amount of follow-up and liaising often carried past the usual 8-5pm working hours as I needed to keep up the communications with overseas colleagues often till midnight.

This was further compounded when the lockdown lifted in Mid June 2020 when projects that were halted during the lockdown were suddenly requested by customers (with shorter timeframes/deadlines). The silver lining above all these busyness was that the industry I am in is still proving to be resilient in the face of recession so far. This is despite my parent company suffering and having retrenchment exercise. It has so far not spilled over to my company (yet).

2. Isolation/ Managerial changes has been tough for me

When I was getting into the rhythm of the new normal, something else hit like a truck. The manager who is currently in charge of me and who was the mentor/manager who hired me suddenly announced his retirement.

Now, I am unsure what were the reasons behind his retirement. It could be that the company also took the chance to reduce cost, but the official reason was to go back to his family and enjoy an early retirement.

What this meant for me is that I felt much of the work I've done is now going to go unrecognized for the new incoming manager who is stationed halfway around the globe. I fear for my future role at work now that my "backing" is gone and that has brought about alot of anxiety at work.

Because often at work - we really work for our immediate managers.

So, here I am again: Back to the drawing board

I am finally now able to take a step back to clear leave, take a breather and re-align. After much reflection, I guess I have the following choices:

- Default position: Stay on and win the trust of the new manager. Continue to deliver

- Start looking out for new opportunities: There have still been some decent enquires received on LinkedIn. Unfortunately, I have not stayed in a single position for more than 2 years in my last 3 jobs (voluntarily and involuntarily).

From my last post, I have only added YZJ Shipbldg (SGX:BS6) at $0.985. This was because in spite of the pandemic, YZJ has still secured business.

Quoting this article in 30 April 2020: "As at 31 March 2020, Yangzijiang sat on an orderbook of $2.9bn for 69 vessels, excluding the 157,000-dwt tanker. The orders are expected to keep the yards at a healthy utilisation rate up to late-2021 and provide a stable revenue stream for at least the next 1.5 years."

|

| https://www.seatrade-maritime.com/shipbuilding/yangzijiang-bags-seven-newbuilding-orders-worth-360m-q1 |

As the time of writing today on 2nd November 2020, its recovery in June has quickly given way to uncertainties in the wider global market on the backdrop of US elections, and the fears of second waves of Covid-19 in US and Europe.

|

| YZJ chart from point of entry back in May 2020 (Blue arrow) |

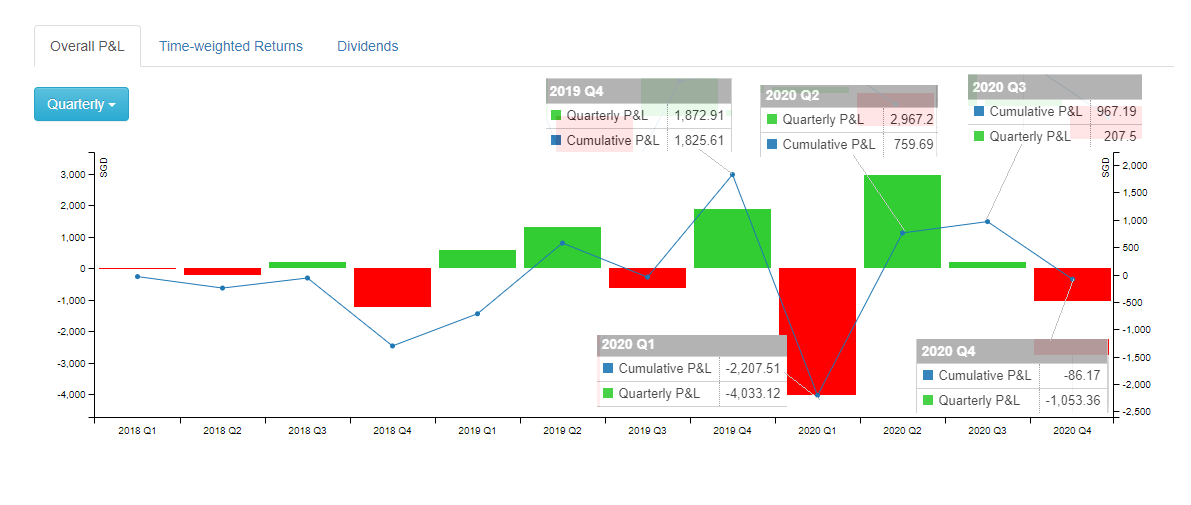

1. Portfolio Update 2nd November 2020.

I am now relying on Stocks Cafe to quickly track my portfolio. It saves me time to compute individual stock returns and I am able to focus on tracking my expenses and savings rate. I still do run my own portfolio tracker and tabulate it once a month.

However, Stocks Cafe does give quick analysis tools that I find helpful to track the progress of my portfolio.

|

| The Covid-19 has seen a sharp drop, with share recovery but now fallen back into negative zone. |

2. Stocks watch (US elections/ Covid-19 wave 2) - SReits

I am now currently watching the market for opportunities as many of the SGX counters are down and it could present a new opportunity to accumulate shares again (like what happened in March 2020). The Singapore market has barely recovered and it has since become the worst performing stock market in Asia.

Overall market is still in down trend but it presents opportunities to buy in counters that are trading at discount from their recent highs.

Of course, the talk of town all over the papers is about Robinson's closure. According to a Straits Times article on 31st October 2020, they have been making losses for at least the past 6 years. The following reasons were cited:

- Increase of heartland malls (more competition/less traffic)

- Onslaught of online businesses.

- Covid-19 impact (but it is recognised that they were already struggling before Covid)

|

| Source: https://www.straitstimes.com/business/companies-markets/singapore-reits-exposure-to-robinsons-owner-in-spotlight-as-fashion |

There have been many netizens pointing fingers at the "Landlords", and that REITs are evil for being money suckers. However, I think these are knee jerk reactions. In the past, we've seen many departmental stores close down as well. Mr Market run in cycles and unfortunately, it seems we are at the end of a business and economic cycle brought about by Covid-19.

Before Robinsons, there was John Little, Carrefour, Duty Free, Metro, Forever 21 that closed. Did these companies close because of high rentals alone? I don't think it is essentially the government's job to bail out companies like these (but do note that the government did in fact try to help wage supplement with all the packages to hep soften the blow to Singaporeans).

Also, retail malls would have to evolve to stay relevant to changing consumer habits. There are also blogshops like Love Bonito that open brick and motar shop to better reach its consumers. Why isn't the traditional departmental store model working out? Businesses will have to keep evolving to stay relevant. Meanwhile, malls may change to incoporate more eateries (as have been an observed trend over the years)

This won't be the last closure we are seeing anytime soon for sure as the group that owns Robinsons also own other brands like Marks & Spencer, Zara and Mango.

SReits in spotlight due to Robinson's exposure

I believe that these malls would no doubt recover over time. The question remains only to answer is how long these Covid-19 restrictions and fear would prolong plus how would the market recover as new tenants take over the vacated spaces. This in turn means that if we are to buy in, we would need holding power to stomach further potential losses to reap the potential gain when it recovers.

This means we need to have a high saving % to be able to deploy money we would not need in the immediate future for survival (with emergency fund).

1. CapitaMall Trust (SGX: C38U) has changed name to CapLand IntCom T (SGX: C38U) - largest exposure to the group by store count with 15 outlets. Trading at $1.76 which has dropped off from recent $2.00 levels. Of course the parent CapitaLand (SGX: C31) is also affected.

2. Frasers Cpt Tr (SGX: J69U) - second largest exposure with 11 outlets.

3. Other counters affected potentially by links to the Al-Futtaim brands:

- StarhillGbl Reit (SGX: P40U) - Ngee Ann City, Wisma Atria

- Lendlease Reit(JYEU.SI) - 313@somerset

- Mapletree Com Tr(N2IU.SI) - VivoCity

Likewise, these counters have seen their stock prices dropped (but these were more on the backdrop of fear of Covid wave 2 on the global scene and US stimulus talks).

Every 危机 (danger) also represents 转机 (opportunity). Wishing all friends and investors good health amidst this global pandemic as it drags on.

1. Why you need to set aside money for savings first

2. Interview process cycle: How to increase your interview rates

3. I'm retrenched: 3 things to think about

Disclaimer: The views expressed, opinion and information in this article are strictly for informational purposes to encourage educational discussions only. No content on this site constitutes - or should be understood as constituting - a recommendation to enter any securities transactions or to engage in any of the investment strategies presented in our site content. We do not provide personalised recommendations or views as to whether a particular stock or investment approach is suitable to the financial needs of a specific individual. No representation or warranty expressed or implied is made as to, and no reliance shall be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained on this website. "30 Year Old Investor" shall not be liable whatsoever for loss or damages of any kind arising from the result of any use, reliance or distribution of the articles or its contents from information contained on this website.